CWS Market Review – September 21, 2021

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year.)

Before I get to today’s newsletter, I want to mention that today is our ETF’s fifth birthday. The AdvisorShares Focused Equity (CWS) started trading five years ago today. Over that time, we’ve nearly doubled investors’ money, and we’ve done it with low turnover and a long-term focus.

Lots of ETFs fold each year but we’re still going strong. Thanks to everyone for your support and here’s to many more years!

The Market Stumbles

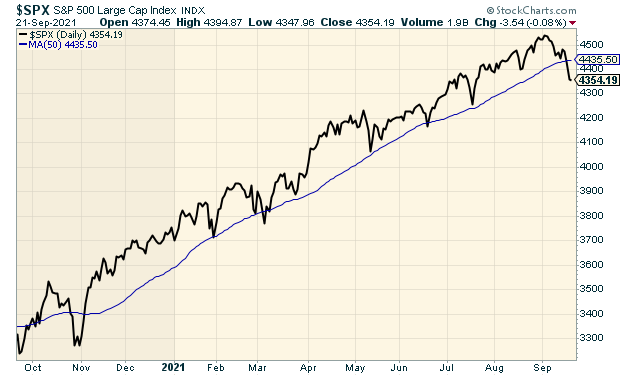

Yesterday, the stock market suffered its worst loss since May. To be honest, the drop wasn’t so bad. By the closing bell, the index shed 1.70%. For some context, we had 31 days worse than that last year, which admittedly was an unusual year.

When I say that yesterday was the worst day in over two months, that really says more about the last two months than it does about today. The true market outlier wasn’t yesterday’s drop but how calm the market has been for the last several weeks. In fact, yesterday’s market was cushioned by a late-day rally. At one point, the Dow was down 971 points, and the S&P 500 was off by 2.87%. We were down again today, but only by a small bit.

Yesterday’s market was also a near-perfect environment for our Buy List to outperform the rest of the market. All told, our Buy List lost 0.97% yesterday. That’s a big outperformance for our portfolio which is well diversified.

The reason we did so well in a relative sense is that our Buy List is concentrated in many high-quality conservative stocks. Five of our stocks actually closed higher yesterday while 19 of our 25 stocks beat the market.

Let me stress that one-day performance doesn’t tell us how good a portfolio is. Instead, I mean to say that our portfolio is designed to do better under certain conditions. To be fair, there are days when our kinds of stocks are on the outs. That’s simply how the market works. To everything, there is a season. It always sounds odd to talk about outperformance on a down day, but I’ve found that the best portfolios really make their mark during tough markets.

Bloomberg said that yesterday, the 500 richest people in the world lost a combined $135 billion. Elon Musk lost $7.2 billion. The poor chap is no longer a $200 billionaire. Yesterday was also the first time that the S&P 500 closed below its 50-day moving average on back-to-back days since last October. That’s the longest such streak in 25 years.

If you’re not familiar with the 50-day moving average, it’s simply the average closing price for the last 50 trading days. There’s also a 200-day version, plus others. I like to think of the 50-DMA as a stupid metric that works for very smart reasons.

Why is this so? The stock market tends to be trend-sensitive. A rising market will generally tend to keep rising and a lousy market will tend to stay lousy. That sounds obvious, but there’s a lot of complicated math behind it. Usually these trends will last longer than you or anyone thought possible.

That means that the big events in the markets are the turning points. Spotting them, however, is notoriously difficult. Make that impossible. That’s where the 50-DMA comes in. It’s a dumb metric but it does give you a general sense of where you are vis-à-vis the current trend.

The 50-DMA won’t pick the exact bottom, but it will turn not long after, and it will turn earlier if the turn is more dramatic. During last year’s market panic, the S&P 500 jumped above its 50-DMA about one month after the low.

There’s a very general rule of thumb that after big days, the market will perform one-third of the opposite of what it just did. So a drop of 1.7% will be followed by a rise of 0.57%. Early on today, it looked like we were going to heed close to the rule, but the market sagged into the close. The stock market closed lower again today, but this time by just 0.08%.

Another Lehman Brothers Moment?

So what caused the market to stumble? The most prominent reason is that a Chinese real estate company called Evergrande is about to go kablooey. Some folks are talking about it being a “Lehman moment” akin to when Lehman Brothers went under 13 years and one week ago.

Evergrande is a highly reckless company that gorged on debt. The company now owes $300 billion. There’s a famous quote from John Paul Getty: “If you own a bank $100, that’s your problem. If you owe the bank $100 million, that’s the bank’s problem.” I’d add that if you owe the bond market $300 billion, that’s the global financial system’s problem. The WSJ said that Evergrande was paying off suppliers with unused real estate properties.

Evergrande was the kind of company that found itself in the right place at the right time. The company made affordable housing that met the demands of China’s growing middle class. From the WSJ: “It expanded into theme parks, healthcare services, mineral-water production and electric-vehicle manufacturing. It enlisted Hong Kong actor Jackie Chan at one point to help promote its bottled water.”

For its part, Beijing seems completely uninterested in any sort of bailout. I hate to think that the Communists do capitalism better than we do. In fact, Evergrande’s recent problems have been quickened by the Chinese government’s push against speculation. The government didn’t like it when home prices soared out of the reach of so many workers.

Here’s Evergrande’s stock chart:

Yuck! The problem with these kinds of problems is that you’re never exactly sure who’s exposed to the risk. Company A may go bust and it can be a terrible company. Company B may be a very good company but it loaned Company A way too much money. Now Company B is in trouble. Then if Company B starts to rattle, you don’t know who was exposed to them, and so on. In no time, you can have a chain reaction that freezes world finance.

I’m sure you’ve heard of the Butterfly Effect. This is the idea that one small event on one side of the world have can have a major impact, weeks later, on the other side of the world. Global finance is like the Butterfly Effect just faster and with more money.

In the 1990s, there was a very successful hedge fund called Long-Term Capital Management. It was full of a lot of eggheads who used their models to make tons of money. The problem is that models can only get you so far in finance. LTCM made a big bet on Russia. They assumed that Russia would never default on its debt. After all, that’s something that had never happened with a nuclear power. That is, until it did. Russia defaulted and LTCM got totally wiped out. It all happened in a few days.

The problem for the Fed was that half of Wall Street had lent them money. At one point, the fund was worth $4.7 billion. After they went bust, Warren Buffett offered to buy LTCM for $250 million. He gave them one hour to decide. Ultimately, a group of Wall Street banks got together to bail them out (no government money was used).

Investors outside of the United States have become used to news emanating from New York and Washington driving capital markets. Perhaps for the first time, American investors will have to stand and watch what’s happening in China. I don’t know if the Chinese economy is in trouble, but Wall Street economists have been cutting their forecasts for Chinese GDP growth. That means tourism in the U.S. I noticed that shares of Disney (DIS) were down over 4% today.

It’s all connected, so said the butterfly.

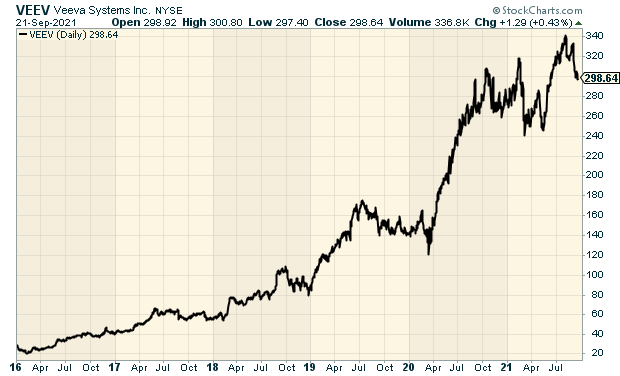

Stock Focus: Veeva Systems

I like to say that the only thing better than owning a monopoly is owning a near-monopoly. After all, the real thing tends to draw too much attention.

That leads to me this week’s stock which is Veeva Systems (VEEV) of Pleasanton, CA. While Veeva isn’t technically a monopoly, it enjoys many of the advantages that a monopoly has. Veeva is a cloud-computing company that’s focused on pharmaceutical and life sciences industry applications. The company was founded in 2007 by Peter Gassner and Matt Wallach. Gassner has become a billionaire along the way and he currently serves as CEO.

What Veeva does is help drug companies capture clinical trial data and follow regulations while letting their sales forces to be more effective. The company has been very successful. Veeva recently became the fifth SaaS (software-as-a-service company) to join the billion-dollar revenue club. The key is that Veeva brings the benefits of cloud computing to a single industry.

This is a critical time for Veeva due to Covid-19. Running all those clinical trials normally involves visiting doctors and researchers. Veeva allows that to happen virtually, which places Veeva’s services in great demand. A particular strength is that Veeva helps its clients comply with government regulations.

I have to confess that watching Veeva has become somewhat entertaining because Wall Street consistently predicts that Veeva’s remarkable run is about to come to an end. Yet each quarterly earnings report easily dispels that notion.

The last report was especially good. On September 1, Veeva said that total revenues for Q3 jumped 29% to $455 million. Not bad. A key stat is that subscription revenue increased by 29% to $366 million. That’s a very good number. All things being equal, I prefer to see a company with strong recurring revenue.

Quarterly earnings came in at 94 cents per share. That beat Wall Street’s forecast by seven cents per share. Veeva has now beaten Wall Street’s consensus for at least the last 32 quarters in a row. (It could be even longer, but that’s as far back as my data goes.)

In the earnings report, Veeva also offered guidance for Q3 and the rest of the fiscal year. For the current quarter, ending October 31, Veeva sees revenues ranging between $464 and $466 million. The company sees earnings of 87 to 88 cents per share. That’s a small range which I take to be a hint.

For the full fiscal year which ends on January 31, Veeva projects revenues of $1.830 to $1.835 billion, and earnings of $3.57 per share. While that’s an optimistic forecast, it didn’t satisfy everyone.

Like I said, Veeva has been ganged up on more than once by a nest of short-sellers. Their mantra has been, “Sure, Veeva’s had some impressive growth until now but the total addressable market isn’t that large.” I think that’s way off-base. In fact, I think cloud is only the beginning.

Now let’s get to some truly remarkable stats. Veeva maintains gross margin in excess of 70%. That’s very impressive. Their operating margins are consistently over 25% and the company doesn’t carry any long-term debt. That’s a testament to how strong a position Veeva has in its market. Peter Gassner has referred to Veeva as having delivered what he calls “30/30” quarters, meaning 30% growth and 30% operating margins.

The stock has been a phenomenal winner (see the chart above). Five years ago, you could have picked up one share of VEEV for $40. Lately, VEEV has traded near $300. That’s quite a run.

While I like Veeva a lot, I’m not a fan of the share price. It’s run too far too fast. Even if we assume the company’s optimistic forecast is correct (and it probably is), that means Veeva is currently trading at 83 times this year’s earnings estimate. That’s about four times what many other stocks go for.

I understand the need to pay for growth, but investors must keep things in perspective. Even if Veeva continues to cream estimates, the stock is still very pricey. Veeva Systems is definitely a stock to watch, but it’s not even close to being a buy until it’s close to $150 per share. Even that is still pretty rich.

– Eddy

P.S. If you haven’t had a chance, you can subscribe to our premium newsletter. It’s only $20 a month or $200 a year. Please join us!