CWS Market Review – June 24, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Wall Street seems pleased that the Twelve Day War is, hopefully, behind us. On Tuesday, the stock market gained nearly 1% on Monday and just over 1% on Tuesday. The index closed at its highest level in four months, and now we’re only 0.85% away from a new all-time high.

Historically, the market has sold off when wars start. In fact, 75 years ago tomorrow, North Korea stormed into South Korea and the Dow plunged 5%. That was the worst day for the market between 1937 and 1962.

This time, it looks like a lot of investors stayed on the sidelines until the geopolitical news was more certain. All the folks who bet on a spike in oil prices didn’t get what they hoped for. On successive days, the price for oil fell by 7% and then by 6%. Oil is cheaper now than where it was before the conflict.

Today, Fed Chairman Jerome Powell headed down to Capitol Hill for his semi-annual testimony before the House and Senate. (Several years ago, I went to the Senate office building to check out the hearings live. I managed to get the seat directly behind Ben Bernanke.)

While it’s broadly assumed that the Fed will cut rates in September, there’s been growing pressure on the Fed to make a move earlier than that. The pressure is coming from many different sources. Most principally, President Trump is clearly frustrated that the Fed hasn’t yet lowered rates.

At his testimony, Powell said that the economy is doing well and that the labor market is strong, but the sore point is inflation which is still above the Fed’s target range of 2.4%. Still, that’s near the lowest point it’s been in the last four years.

This is what Powell had to say about inflation:

Inflation has eased significantly from its highs in mid-2022 but remains somewhat elevated relative to our 2 percent longer-run goal. Estimates based on the consumer price index and other data indicate that total personal consumption expenditures (PCE) prices rose 2.3 percent over the 12 months ending in May and that, excluding the volatile food and energy categories, core PCE prices rose 2.6 percent. Near-term measures of inflation expectations have moved up over recent months, as reflected in both market- and survey-based measures. Respondents to surveys of consumers, businesses, and professional forecasters point to tariffs as the driving factor. Beyond the next year or so, however, most measures of longer-term expectations remain consistent with our 2 percent inflation goal.

Powell’s concern is that President Trump’s tariff policies will heat up inflation but even that is unclear. The problem is that Powell is warning us of something we don’t yet see. As a result, his conservative approach appears overly cautious.

President Trump said he hopes “Congress really works this very dumb, hardheaded person over.” I agree that the Fed is probably unnecessarily hawkish on interest rates. The Fed can easily afford to cut rates by 0.25% next month.

Here’s a look at the “real” Fed funds rate, meaning the after-inflation rate. I used the “core rate” of inflation because I think that presents a more accurate view.

Real rates are currently at 1.5%. There’s plenty of room to cut before real rates turn negative.

Before the Financial Crisis, the Fed’s job was easy: set real rates around 3% or so when the economy is humming along and drop real rates to 0% when a recession is coming. I’m exaggerating, but that pretty much captures what happened. The Financial Crisis rewrote the rules and now we see that real rates can go below 0% for a long time.

Powell also faces the dual concern that we don’t know what the tariff policy will be, nor do we know what the outcome will be. Historically, tariffs have led to one-time price hikes and not to persistent inflation like we saw in the 1970s.

Powell’s term as Fed chair is up next year. President Trump seems to favor making Scott Bessent, his Treasury Secretary, the next Fed chair.

There could be growing dissension within the Fed. Recently, two Fed governors, Michelle Bowman and Christopher Waller, have signaled that the Fed can cut rates soon. While Fed bank presidents have been known to deviate from the Fed chair, it’s rare for Fed governors to dissent.

For the July meeting, futures traders think there’s only a 19% chance that the Fed will cut. That sounds about right. For September, traders see an 82% chance that the Fed will cut.

On Thursday, the government will update its report on Q1 GDP. This will be the second revision to the report. The most recent revision said that the US economy contracted by 0.2% during the first three months of this year. That was the first negative quarter for GDP since 2022.

There’s a growing consensus on Wall Street that the economy did much better during the second quarter. Some forecasters think the economy grew over 3% in real terms during the second three months of this year.

Now let’s look at our sole Buy List earnings report from yesterday.

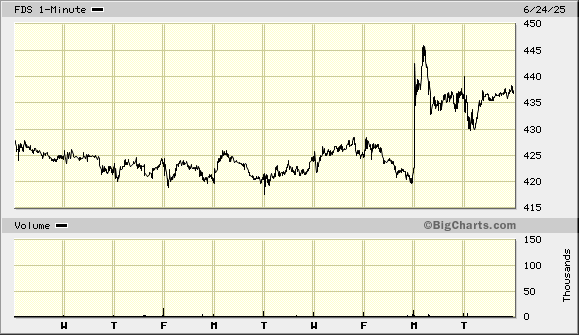

FactSet Misses Earnings but Rallies

Before yesterday’s opening bell, FactSet (FDS) reported its fiscal Q3 earnings. I’ll go into more details in our premium letter later this week, but I wanted to touch on a few points.

I also wanted to mention FactSet because there was some misunderstanding about the report. Technically, FactSet fell short of Wall Street’s estimate. For the quarter, FactSet made $4.27 per share which was three cents below consensus.

However, the details of the report were quite good. Don’t take my word for it. Shares of FDS gapped up yesterday. At one point, FDS was up more than 5.5% on the day. The stock is up more than 10% from its April low.

Business is still going well for FDS. The problem is that costs have been weighing it down. Last quarter, revenues rose by 6%, and organic revenue was up by 4.4%.

The key stat for FDA is annual subscription value (ASV). Last quarter, ASV grew by 6%, The ASV retention rate is higher than 95%.

The board approved a new $400 million share buyback program. FactSet has reduced its share count by more than 8% over the last 10 years. Like I said before, I’ll have more to say about FDS in our premium issue, but the company is doing well. FDS recently raised its dividend for the 26th year in a row. I expect more gains later this year.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy