CWS Market Review – June 10, 2022

“It is better to be roughly right than precisely wrong.” ― John Maynard Keynes

The S&P 500 closed Thursday at a two-week low. As far as market moves go, that’s not so terrible, but it appears as if the latest bear-market rally has run out of gas. Or maybe it can’t afford more gas—in which case, it’s just like everybody else.

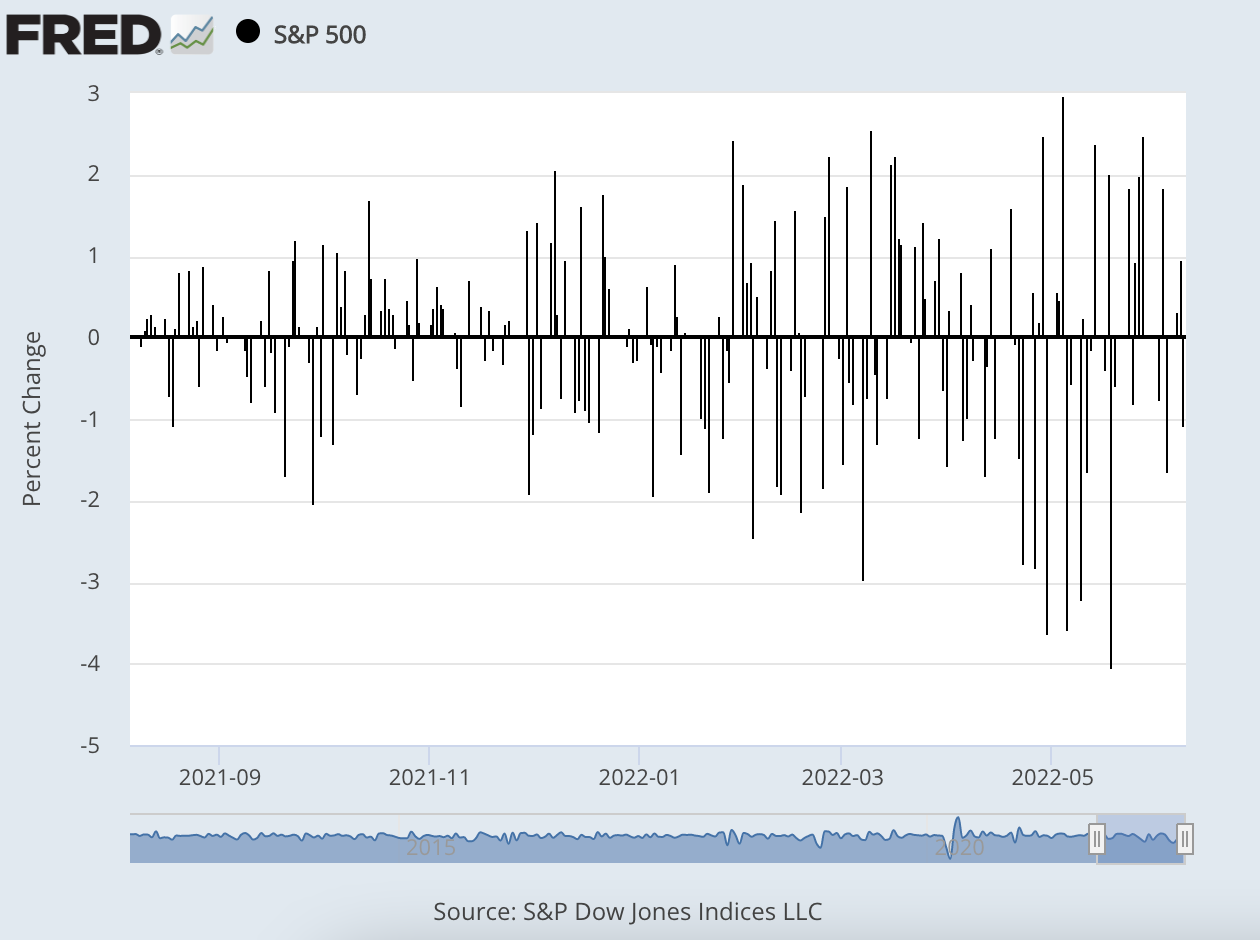

Truthfully, this is how bear markets work. Investors see a lot more volatility combined with false breakouts. Thursday was the 20th time this year that the S&P 500 had a daily change, up or down, of more than 2%. Last year, it only happened seven times.

Here’s a look at all the daily changes for the S&P 500 over the last several months. Notice how the changes have gotten progressively more pronounced:

The major issue plaguing the market and economy continues to be inflation. I’m writing this to you early on Friday. Later this morning, the latest inflation report comes out, and it will most likely show more bad news. This transitory inflation is certainly taking its sweet time.

I’ve been very critical of the Federal Reserve recently, and it’s hard not to be. Inflation is a cruel tax that falls mostly on the poor and many seniors who live on a fixed income. It needs to be fought aggressively.

The Fed meets again next week, and it’ll almost certainly hike rates by 0.5%. It’s not close to being done. Following next week’s hike, I expect 0.5% hikes at the next two meetings, and there could be a third before the end of the year, but that might come after Election Day.

It’s not all bad news. We had some good news this week from our Buy List. SAIC reported very strong earnings. The company also raised guidance, and the shares jumped 7% on the news. The stock came within a hair’s breadth of a new 52-week high. SAIC is now our #1 performer this year. I’ll have all the details in a bit.

Before we get to that, I want to address a question that I’m currently hearing more of.