CWS Market Review – July 1, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

It finally happened! On Friday, the stock market closed at a new all-time high. The index rose even higher yesterday and closed above 6,200. The market closed a tad lower today. Still, over the last 12 weeks, this was one of the fastest rallies in recent market history.

For some context, the index last closed below 6.2 on August 2, 1932. That means that the stock market has gained 1,000-fold over the last 93 years.

As bear markets go, this was one of the quicker ones. The S&P 500 peaked at 6,144.15 on February 19. Interestingly, that was five years to the day since the Covid peak in 2000.

Thanks to the Trade War hysteria, by April 8, the S&P 500 fell to 4,982.78. Since then, the market has powered itself upward, and daily volatility has collapsed.

This is a good lesson in why it’s important to avoid timing the market. The stock market can act in a manic manner, especially in the short-term. That’s why the best strategy is to buy and hold high quality stocks.

Speaking of which, I’m happy to report that our Buy List beat the market again for the first half of this year. Through Monday’s close, our Buy List was up 7.90% for the year. Meanwhile, the S&P 500 gained 5.50%.

One quick note to that. The return I listed doesn’t included dividends. For my year-ending stats, I always include dividends. As you know, I believe that dividends are very important to any long-term portfolio. I just didn’t have enough time to calculate the dividend-adjusted returns.

The dividend yield of the Buy List is usually very close to the yield of the S&P 500. For the first half of this year, the S&P 500 dividend adjusted return was 6.20%, so dividends added 60 basis points to the total return of the market. My rough estimate is that dividends added about 50 basis points, give or take, to the total return of our Buy List. The bottom line is that we’re beating the market.

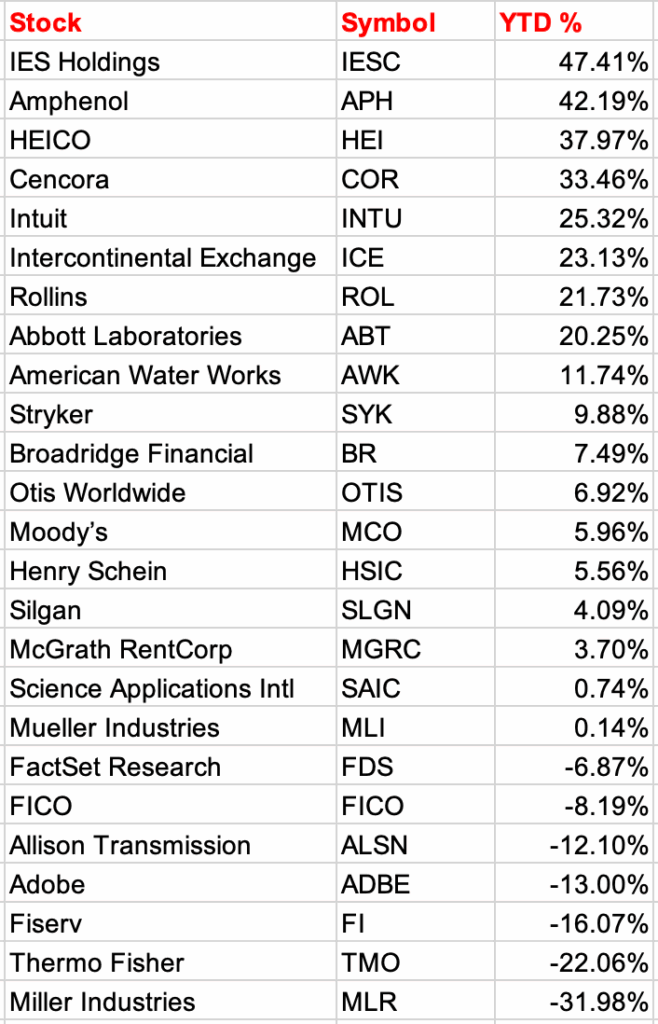

Here’s a list of all 25 stocks and how they’re doing so far this year through Monday’s close:

One stock I want to highlight is Heico (HEI) because our patience is paying off. This is a wonderful company that still isn’t very well known. Heico is the kind of niche business I love. With investing, the only thing better than a monopoly is a near-monopoly. (The full-on monopolies tend to get too much government attention.)

Heico makes replacement parts for the airline industry. If a commercial aircraft needs some obscure new part, the airline can’t run down to the local hardware store. Instead, it needs to special-order it. Moreover, there’s a great deal of cost pressure on the airlines to keep the older planes serviceable.

Also, the aircraft parts often need to meet strict regulatory guidelines. The part maker really has to know what it’s doing. That’s where Heico comes in. The business is lean and well-run.

Check out this 30-year chart:

I can’t tell the Heico story without mentioning the Mendelson family. Larry Mendelson is the current chairman and CEO. In the 1950s, he took a finance class taught by David Dodd. Fans of value investing will recognize Dodd’s name. He was the co-author of Security Analysis with Ben Graham. Security Analysis is probably the foundational text of value investing.

Mendelson took those lessons to heart. He made a good deal of money in real estate and wanted to diversify his holdings. That led him to invest in an under-performing industrial company. He really didn’t care what he bought, as long as it was cheap and had potential to be retooled for future growth. He chose well.

Heico was originally founded in 1957 by Dr. William Heinicke as Heinicke Electronics. By the 1980s, Mendelson controlled a sizeable share in the company and was able to make himself CEO. The Heinicke family still owns a large chunk of the voting shares, and several family members hold key positions within the company.

When airplane owners need a new part and go back to the original equipment manufacturer (OEM) to get replacements, they’re often charged a steep price. The profit margins can exceed 30%. That provides enormous opportunity for Heico. Consider that many aircraft are over 20 years old.

The aviation industry is broadly diversified, and Heico is also able to get sales from commercial and military customers. That means that if there’s a drop-off on one end of the business, the other side can pick up the slack. Wherever there’s a demand to cut costs, Heico has the potential to do well.

In some respects, I see Heico’s role as similar to that of a generic drugmaker. Heico provides a low-cost copy of the original product, which is regulated by the Federal Aviation Administration. By the way, Heico does more than aircraft parts. They also supply parts for satellites, rockets, missiles and even medical instruments.

Last November, HEI peaked at $283 per share. After that, the stock ran into a lot of bad luck. Much of that could have been DOGE-related. Then in December, the shares took a 9% bath after HEI’s earnings report didn’t please Wall Street traders (they beat by one penny).

While I was unhappy with the falling price, I decided to keep Heico on our Buy List for this year. The stock continued to fall. By February 19, shares of HEI reached $216 per share. That was the same day the broad market peaked. A few days later, Heico released a very good earnings report ($1.20 vs. 95-cent estimate).

Since April, Heico has been in rally mode. It took time, but we made back everything we lost. The shares have recently been as high as $328 per share. Through yesterday, HEI is up 38% for us.

A few weeks ago, Heico reported another solid quarter. Heico reported fiscal-Q2 earnings of $1.12 per share. That’s up from 88 cents per share for last year’s Q2, and it beat Wall Street’s consensus of $1.03 per share.

Net sales increased 15% to a record $1,097.8 million. Operating income rose 19% to $248.2 million, and operating margin improved by 70 basis points to 22.6%. Mendelson said, “We continue to forecast strong cash flow from operations for fiscal 2025.”

For Q2, the Flight Support Group had net-sales growth of 19% and operating-income growth of 24%. The group has now delivered 19 straight quarters of sequential sales growth. Electronic Technologies had net-sales growth of 7% and operating income was up 3%. Heico is due to report earnings again in late August.

Before I go, I wanted to mention that earlier today, Jerome Powell said the Fed would have cut rates already had it not been for the tariffs. That remark may have been what sparked an unusual market on Tuesday. Industrial stocks did very well, but tech was a laggard.

Even though the S&P 500 closed lower on Tuesday, the Dow added 400 points. You don’t often see spreads like that. This could be the market adjusting to Powell’s remarks. President Trump continued his criticism of Powell and called him a “moron.”

The S&P 500 Equal Weight Index closed higher by more than 1.1%. The S&P 500 Growth Index closed down by 1% while the S&P 500 Value Index rose by 1%.

The S&P 500 Industrials Index rose by 2.28% and the S&P 500 Tech Index was down by 1.13%. I wouldn’t be surprised if this rotation lasts for a few weeks. The odds now say the Fed will cut rates by 1% before the end of the year.

This will probably be a quiet week. The stock market will close early on Thursday, and it will be closed all day on Friday in honor July 4th. The June jobs report is due out Thursday morning. Wall Street expects that only 100,000 jobs were created last month.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy